Mastering Budgeting-A Comprehensive Guide to Financial Success

Budgeting is the cornerstone of financial health and stability. Whether you're striving to pay off debt, save for a big purchase, or plan for retirement, having a well-crafted budget can make all the difference. In this guide, we'll delve into what budgeting entails and provide actionable steps to help you create and maintain an effective budget.

What is Budgeting?

Budgeting is the process of creating a plan for how you will allocate your income to cover your expenses, savings, and investments. It serves as a roadmap for your financial journey, helping you to manage your money effectively and achieve your financial goals. A budget allows you to track your spending, identify areas where you can cut back, and prioritize your financial objectives.

How to Do Budgeting:

1. Determine Your Financial Goals:

Before creating a budget, it's essential to define your financial objectives. Whether you want to build an emergency fund, pay off debt, save for a vacation, or invest for retirement, having clear goals will guide your budgeting decisions.

2. Calculate Your Income:

Start by determining your total monthly income. Include all sources of income, such as salaries, bonuses, freelance earnings, and investment returns. Having an accurate picture of your income is crucial for creating a realistic budget.

3. List Your Expenses:

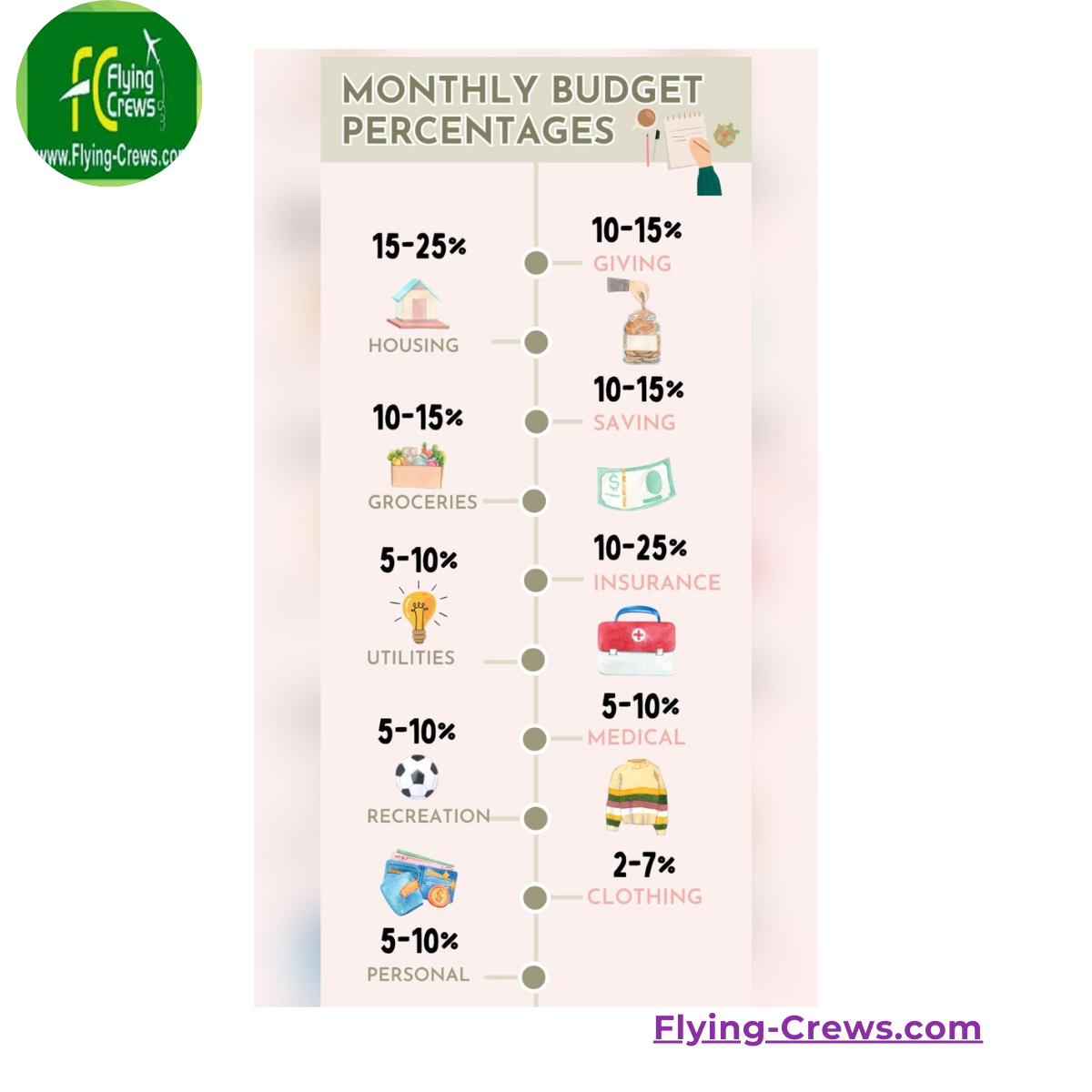

Next, make a list of all your expenses. Categorize them into fixed expenses (e.g., rent/mortgage, utilities, insurance) and variable expenses (e.g., groceries, dining out, entertainment). Don't forget to include periodic expenses like annual subscriptions or quarterly bills.

4. Differentiate Between Needs and Wants:

Differentiating between needs and wants is key to effective budgeting. Needs are essential for survival and include things like housing, food, and healthcare. Wants, on the other hand, are non-essential items or activities that you can live without. Prioritize your needs in your budget while allocating a portion of your income to wants.

5. Set Spending Limits:

Based on your income and expenses, set spending limits for each category. Be realistic and ensure that your spending aligns with your financial goals. Remember to leave room for unexpected expenses and emergencies by building an emergency fund.

6. Track Your Spending:

Monitoring your spending is crucial for staying on track with your budget. Use tools like budgeting apps or spreadsheets to record your expenses and compare them against your budgeted amounts. Review your spending regularly and make adjustments as needed.

7. Adjust as Necessary:

Life is unpredictable, and your financial situation may change over time. Be flexible with your budget and adjust it as necessary to accommodate any changes in income, expenses, or financial goals.

8. Plan for the Future:

Budgeting isn't just about managing your finances in the present; it's also about planning for the future. Allocate a portion of your income towards savings and investments to build wealth over time. Consider contributing to retirement accounts, setting up automated savings transfers, or investing in low-cost index funds.

Benefits of Budgeting:

- Helps you track your spending and identify areas for improvement.

- Enables you to prioritize your financial goals and allocate resources accordingly.

- Reduces financial stress by providing a clear plan for managing your money.

- Facilitates better decision-making by giving you a comprehensive overview of your finances.

- Sets the foundation for long-term financial stability and success.

Budgeting is a powerful tool for achieving financial freedom and security. By creating a budget tailored to your income, expenses, and goals, you can take control of your finances and work towards a brighter financial future. Remember, budgeting is not a one-time task but an ongoing process that requires dedication and discipline. Start small, stay consistent, and watch your financial goals become a reality.

Mastering Smart Budgeting- Strategies for Financial Success

In today's fast-paced world, traditional budgeting methods may not always suffice. To truly optimize your financial health and achieve your goals, adopting a smart approach to budgeting is essential. In this article, we'll explore what smart budgeting entails and provide actionable strategies to help you create an effective budgeting plan.

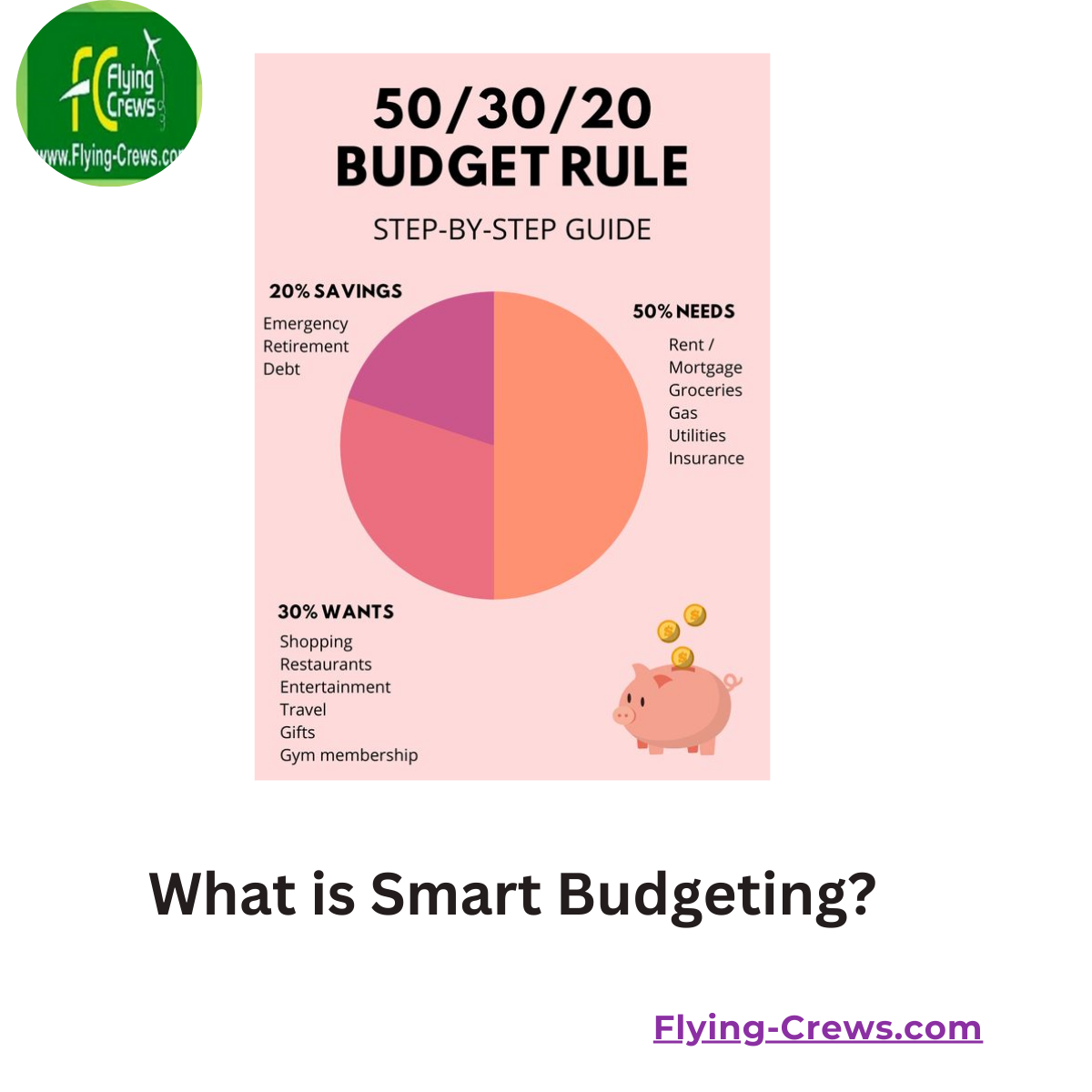

What is Smart Budgeting?

Smart budgeting goes beyond basic income and expense tracking. It involves leveraging technology, behavioral economics principles, and strategic planning to maximize the efficiency and effectiveness of your budget. A smart budgeting approach empowers you to make informed financial decisions, adapt to changing circumstances, and ultimately reach your financial goals faster.

How to Implement Smart Budgeting:

1. Embrace Technology:

- Utilize budgeting apps and software: Take advantage of user-friendly apps like Mint, YNAB (You Need a Budget), or Personal Capital to automate budget tracking, categorize expenses, and receive personalized insights into your spending habits.

- Set up alerts and notifications: Enable notifications for low balances, upcoming bills, or overspending to stay informed and proactive about your finances.

- Use digital payment methods: Opt for digital payment options like mobile wallets or online banking to easily track transactions and streamline your budgeting process.

2. Practice Conscious Spending:

- Identify your priorities: Determine your values and financial goals to align your spending with what truly matters to you.

- Implement the 50/30/20 rule: Allocate 50% of your income to needs, 30% to wants, and 20% to savings and debt repayment. This flexible guideline ensures a balanced approach to budgeting.

- Practice mindful spending: Before making a purchase, consider whether it aligns with your goals and brings long-term value. Avoid impulsive buying and focus on mindful consumption.

3. Automate Finances:

- Set up automatic transfers: Automate your savings contributions, debt payments, and investment contributions to ensure consistency and discipline.

- Schedule bill payments: Use autopay features to schedule recurring bill payments and avoid late fees or missed payments.

- Implement direct deposit: Arrange for your paycheck to be directly deposited into your bank account to streamline cash flow management and avoid unnecessary trips to the bank.

4. Track and Analyze Your Finances:

- Monitor your spending trends: Regularly review your budget and analyze spending patterns to identify areas for improvement and potential cost-saving opportunities.

- Conduct periodic financial check-ins: Schedule monthly or quarterly reviews to assess your progress towards financial goals and adjust your budget accordingly.

- Leverage data analytics: Use budgeting tools to generate reports and visualize your financial data, allowing for deeper insights and informed decision-making.

5. Adapt and Evolve:

- Remain flexible: Life is dynamic, and your financial circumstances may change over time. Be prepared to adjust your budget as needed to accommodate new goals, income fluctuations, or unexpected expenses.

- Continuously seek optimization: Explore new budgeting strategies, tools, and techniques to enhance your financial management skills and maximize your resources.

Benefits of Smart Budgeting:

- Streamlines financial management processes and reduces administrative burden.

- Promotes conscious spending and empowers you to make informed financial decisions.

- Facilitates goal achievement by prioritizing resources towards meaningful objectives.

- Enhances financial awareness and accountability through regular tracking and analysis.

- Fosters adaptability and resilience in the face of changing economic conditions or life circumstances.

Smart budgeting is a proactive approach to financial management that leverages technology, behavioral psychology, and strategic planning to optimize resource allocation and achieve financial success. By embracing smart budgeting principles and implementing actionable strategies, you can take control of your finances, build wealth, and create a brighter financial future. Start today and unlock the full potential of your financial journey.

10 Essential Financial Budget Plans for Every Stage of Life

Creating a comprehensive financial budget plan is crucial for achieving financial stability and reaching your long-term goals. Whether you're just starting out in your career, raising a family, or planning for retirement, having a tailored budget plan can help you manage expenses, save money, and invest wisely. In this article, we'll explore 10 essential financial budget plans suitable for individuals at various stages of life.

1. Starter Budget Plan (Young Adults):

- Focus on essentials: Allocate the majority of your income towards rent, utilities, groceries, and transportation.

- Prioritize debt repayment: If you have student loans or credit card debt, allocate a portion of your budget towards paying off these obligations.

- Begin saving: Start building an emergency fund by setting aside a portion of your income each month.

- Limit discretionary spending: Be mindful of non-essential expenses such as dining out, entertainment, and shopping.

2. Family Budget Plan (Parents):

- Cover family essentials: Allocate funds for housing, groceries, childcare, and healthcare expenses.

- Save for children's education: Set aside money for college funds or educational expenses.

- Plan for family activities: Budget for vacations, extracurricular activities, and other family outings.

- Consider insurance needs: Include expenses for life insurance, health insurance, and disability insurance in your budget.

3. Debt Repayment Budget Plan:

- Assess debt obligations: List all outstanding debts, including credit card debt, student loans, and personal loans.

- Prioritize high-interest debt: Focus on paying off debts with the highest interest rates first to minimize interest costs.

- Implement a debt repayment strategy: Choose a debt repayment method, such as the debt snowball or debt avalanche method, and allocate extra funds towards debt repayment each month.

- Stay disciplined: Stick to your budget and avoid taking on new debt while repaying existing obligations.

4. Emergency Fund Budget Plan:

- Determine target savings: Aim to save three to six months' worth of living expenses in your emergency fund.

- Set savings goals: Break down your savings target into manageable monthly or quarterly goals.

- Automate savings: Set up automatic transfers from your checking account to your emergency fund to ensure consistent savings.

- Resist temptation: Only tap into your emergency fund for genuine emergencies, such as medical expenses or unexpected car repairs.

5. Retirement Budget Plan:

- Calculate retirement expenses: Estimate your retirement living expenses, including housing, healthcare, transportation, and leisure activities.

- Determine retirement income sources: Consider sources of retirement income, such as Social Security benefits, employer-sponsored retirement plans, and personal savings.

- Develop a retirement savings strategy: Contribute regularly to retirement accounts such as 401(k)s, IRAs, or Roth IRAs to build a substantial nest egg.

- Monitor investment performance: Review your retirement portfolio periodically and adjust your investment strategy as needed to meet your retirement goals.

6. Homeownership Budget Plan:

- Account for homeownership costs: Budget for mortgage payments, property taxes, homeowners insurance, and maintenance expenses.

- Set aside funds for home repairs: Create a separate fund for unexpected home repairs or upgrades, such as roof repairs or appliance replacements.

- Plan for property upgrades: Budget for home improvement projects or renovations to enhance the value and comfort of your home.

- Consider long-term expenses: Anticipate future housing-related expenses, such as HOA fees, landscaping, or renovations for aging in place.

7. Travel Budget Plan:

- Determine travel goals: Identify destinations you'd like to visit and estimate travel costs, including transportation, accommodation, meals, and activities.

- Set a travel budget: Allocate funds for travel expenses based on your destination preferences and travel frequency.

- Use travel rewards: Take advantage of credit card rewards, airline miles, and hotel points to offset travel costs and maximize savings.

- Plan for unexpected expenses: Budget for travel insurance, emergency medical expenses, and unexpected itinerary changes to avoid financial surprises while traveling.

8. Education Budget Plan:

- Estimate education costs: Calculate tuition fees, textbooks, supplies, and other educational expenses associated with pursuing further education.

- Explore financial aid options: Research scholarships, grants, and student loans to help finance your education.

- Create a savings plan: Start saving for education expenses as early as possible by setting up a dedicated education savings account, such as a 529 plan or Coverdell ESA.

- Consider alternative education paths: Explore cost-effective alternatives to traditional higher education, such as community college, online courses, or vocational training programs.

9. Healthcare Budget Plan:

- Budget for medical expenses: Allocate funds for health insurance premiums, deductibles, copayments, and prescription medications.

- Plan for preventive care: Include expenses for routine medical check-ups, vaccinations, and screenings to maintain good health.

- Build a health savings account (HSA): If eligible, contribute to an HSA to save for qualified medical expenses tax-free.

- Consider supplemental insurance: Evaluate supplemental health insurance options, such as dental, vision, or long-term care insurance, to enhance your healthcare coverage.

10. Philanthropic Budget Plan:

- Identify causes and organizations: Determine charitable causes or nonprofits that align with your values and interests.

- Set a giving budget: Allocate a portion of your income or assets towards charitable donations each month or year.

- Research tax benefits: Explore tax incentives for charitable giving, such as deductions for donations to qualified charities or donor-advised funds.

- Get involved: Consider volunteering your time or skills in addition to financial contributions to support causes you care about.

No matter what stage of life you're in, having a well-thought-out budget plan is essential for managing your finances effectively and achieving your goals. By implementing these 10 essential budget plans, you can take control of your financial future, minimize financial stress, and build a solid foundation for long-term success. Remember to regularly review and adjust your budget plans as your circumstances and goals evolve.

Reshma Rajan

HR Manager

Contact details : 9443056013

VCard:

https://reshmarajan.vcardinfo.com/

Linktree :

https://linktr.ee/hrflyingcrew

Linkedin :

https://www.linkedin.com/in/reshma-rajan-a69850176

Pinterest:

https://in.pinterest.com/reshmarajan0516

Quora:

https://www.quora.com/profile/Reshma-Rajan-290

Instagram :

https://www.instagram.com/flying_crews_hr/

Facebook : https://www.facebook.com/profile.php?id=61556299177128

Youtube : https://www.youtube.com/@10BestInCity/videos

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)