*Know Your Customer*

KYC means Know Your Customer and sometimes Know Your Client. KYC or KYC check is the mandatory process of identifying and verifying the client's identity when opening an account and periodically over time. In other words, banks must make sure that their clients are genuinely who they claim to b

What is KYC?

KYC means Know Your Customer and sometimes Know Your Client.

KYC or KYC check is the mandatory process of identifying and verifying the client's identity when opening an account and periodically over time.

In other words, banks must make sure that their clients are genuinely who they claim to be.

Banks may refuse to open an account or halt a business relationship if the client fails to meet minimum KYC requirements.

Why is the KYC process important?

KYC procedures defined by banks involve all the necessary actions to ensure their customers are real, assess, and monitor risks.

These client-onboarding processes help prevent and identify money laundering, terrorism financing, and other illegal corruption schemes.

KYC process includes ID card verification, face verification, document verification such as utility bills as proof of address, and biometric verification.

Banks must comply with KYC regulations and anti-money laundering regulations to limit fraud. KYC compliance responsibility rests with the banks.

KYC documents

KYC checks are done through an independent and reliable source of documents, data, or information. Each client is required to provide credentials to prove identity and address.

In May 2018, the U.S. Financial Crimes Enforcement Network (FinCEN) - added a new requirement for banks to verify the identity of natural persons of legal entity customers who own, control and profit from companies when those organizations open accounts.

Bottom line: when a corporate company opens a new account, it will have to provide Social Security numbers and copies of a photo ID and passports for its employees, board members, and shareholders.

KYC and Customer Due Diligence measures:-

The KYC policy is a mandatory framework for banks and financial institutions used for the customer identification process. Its origin stems from the 2001 Title III of the Patriot Act to provide various tools to prevent terrorist activities.

To comply with international regulations against money laundering and terrorist financing, reinforced Know Your Customer procedures need to be implemented in the first stage of any business relationship when enrolling a new customer.

Banks usually frame their KYC policies incorporating the following four key elements:

1.Customer Policy

2.Customer Identification Procedures (data collection, identification, verification, politically exposed person/sanctions lists check) aka 3.Customer Identification Program (CIP)

4.Risk assessment and management (due diligence, part of the KYC process)

Ongoing monitoring and record-keeping.

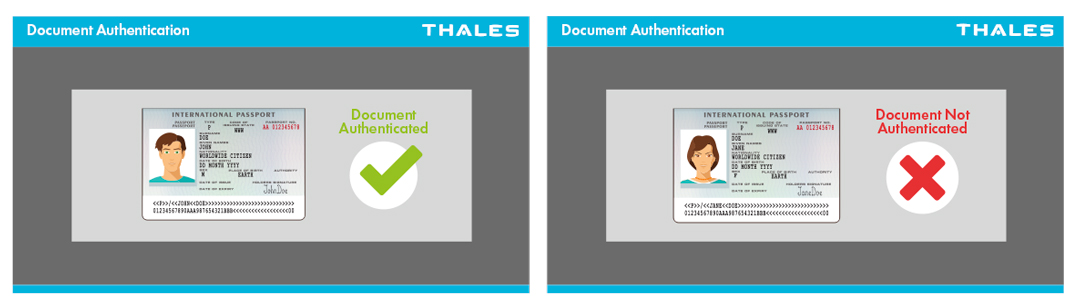

From visual ID check to digital verification

For some, this is still primarily a paper-based check with KYC forms to fill. example:-

For others, it's a digital process that involves verifying that an identity document is genuine or even going further to authenticate the document holder through additional biometric checks such as facial or fingerprint checks.

A digital ID verification process enables a bank to automatically capture customer demographic data, which can be integrated into enterprise systems like CRM to:

1.streamline the customer onboarding process,

2.conduct further due diligence and risk assessment,

3.review for PEPs (Politically Exposed Persons)

Financial institutions must also maintain records on transactions and Information obtained through the Customer Due Diligence measures.

These requirements should apply to all new customers and existing customers based on materiality and risk.

Pranita Jagtap [MBA]

Finance Manager