Analyzing India’s Top FinTech Rivals: PhonePe vs Paytm on Valuation, Technology and Market Dynamics

The FinTech Industry has emerged as one of the most dynamic and transformative sectors in India's Economy, fundamentally reshaping how Financial services are accessed, delivered and consumed. With India's FinTech market valued at $110 billion in 2024 and projected to reach $990 billion by 2032, the sector represents unprecedented growth opportunities. At the forefront of this revolution are two dominant players: PhonePe and Paytm, which together illustrate both the potential and challenges facing India's Digital Financial ecosystem.

Current Valuation Analysis:

PhonePe's Valuation Trajectory –

PhonePe has demonstrated remarkable valuation Growth, evolving from its 2015 founding to achieving a $12 billion valuation in 2023. The company is currently targeting a $15 billion valuation through its planned IPO in 2025, representing a 25% increase from its last private funding round. This ambitious target reflects Investor confidence in PhonePe's market-leading position and growth trajectory.

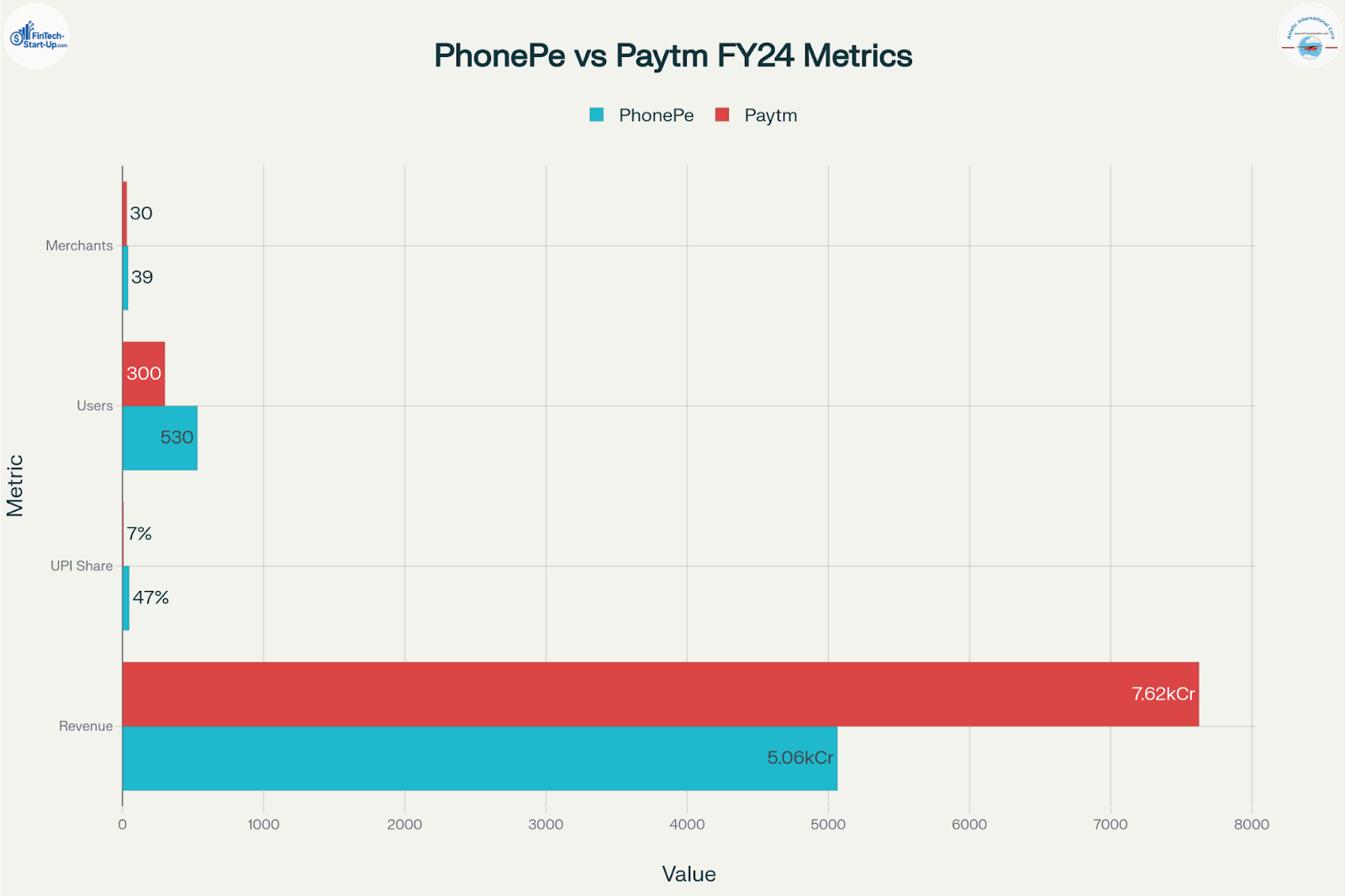

The company's valuation is underpinned by strong operational metrics, including 530+ million registered users and processing over 8.55 billion UPI transactions monthly. PhonePe's dominant 46.5-48% UPI market share provides significant competitive moats and recurring revenue streams.

Paytm's Market Capitalization Dynamics –

As a publicly listed entity since November 2021, Paytm's valuation has experienced significant volatility. The company's current market capitalization stands at ₹64,958 crore (approximately $7.8 billion), representing substantial fluctuation from its IPO pricing of ₹2,150 per share.

Despite regulatory challenges that impacted its revenue decline of 31% in FY24 to ₹7,625 crore, Paytm's diversified ecosystem and established market presence continue to support its valuation. The company's 300+ million user base and extensive merchant network of 30+ million provide substantial value propositions.

Company Size and Scale Comparison:

PhonePe vs Paytm: Key Business Metrics Comparison (FY24)

User Base and Market Penetration –

PhonePe has established a commanding lead in user acquisition, with 530+ million registered users and 250+ million monthly active users. This represents approximately 39% of India's population, demonstrating exceptional market penetration. The platform processes over 250 million daily transactions, highlighting its integration into users' daily Financial activities.

Paytm, while maintaining a substantial 300+ million registered user base, faces challenges in user engagement with 72 million monthly transacting users. This indicates a lower activation rate compared to PhonePe, suggesting opportunities for improved user retention and engagement strategies.

Merchant Network Infrastructure –

PhonePe's merchant ecosystem encompasses 39+ million registered merchants, providing extensive payment acceptance Infrastructure across urban and rural markets. This comprehensive network supports the company's transaction volume leadership and creates significant network effects.

Paytm has deployed 30+ million Soundbox devices and maintains a substantial merchant base. The company's innovative Soundbox technology, launched in 2020, provides competitive advantages in Merchant retention and transaction confirmation, particularly during peak usage periods.

Transaction Volume Leadership –

The scale disparity becomes evident in transaction processing capabilities. PhonePe processes 8.55 billion UPI transactions monthly with a 46.5% market share, while Paytm handles 1.27 billion transactions with a 6.9% market share. This represents approximately a 7:1 ratio in transaction volume, demonstrating PhonePe's market dominance.

Financial Performance Analysis:

Revenue Generation and Growth –

PhonePe achieved impressive revenue growth of 74% year-on-year to ₹5,064 crore in FY24, driven by robust growth in digital payments and financial services. The company's revenue diversification strategy includes financial services contributing ₹207.4 crore, representing 4% of total revenue.

Paytm experienced a revenue decline of 31% to ₹7,625 crore in FY24 due to regulatory disruptions affecting its payment bank operations. However, the company demonstrated resilience through 25% revenue growth to ₹9,978 crore when including UPI incentives and other income.

Profitability Trajectory –

PhonePe achieved a significant milestone by turning adjusted PAT positive with ₹197 crore profit in FY24, excluding ESOP costs. This represents a fundamental shift from losses of ₹738 crore in the previous year, demonstrating operational efficiency improvements.

Paytm narrowed its losses significantly to ₹665 crore in FY25 from ₹1,390 crore in FY24. The company achieved EBITDA before ESOP profitability of ₹559 crore in FY24, marking its first full year of operational profitability since IPO.

Operational Efficiency Metrics –

PhonePe's payment processing charges increased 75% to ₹1,166 crore, reflecting higher transaction volumes. The company has reduced customer service costs by 60% through automation, cutting teams from 1,100 to 400 agents.

Paytm implemented cost optimization measures, expecting annual cost savings of ₹400-500 crore through AI-driven efficiencies and organizational restructuring. The company's contribution profit increased 42% to ₹5,538 crore in FY24.

Future Valuation Prospects:

Growth Catalysts and Market Expansion –

PhonePe's international expansion strategy includes UPI services in Singapore, UAE and pilot programs in multiple countries. The company's diversification into financial services, e-commerce through Pincode and the Indus App Store creates multiple revenue streams beyond payments.

The India FinTech market projection of reaching $990 billion by 2032 at a 30.2% CAGR provides substantial growth opportunities. PhonePe's market leadership position enables it to capture disproportionate value from this expansion.

Regulatory Environment and Compliance –

The NPCI's extension of the 30% UPI market share cap deadline to December 2026 provides PhonePe with continued operational flexibility. However, long-term compliance requirements may necessitate strategic adjustments to maintain market dominance.

Paytm's successful transition from PPBL to partner banks demonstrates regulatory adaptability and creates new monetization opportunities through banking partnerships. This transition reduces regulatory risk while expanding revenue potential.

Technological Innovation and Competitive Positioning –

Both companies are investing heavily in AI and machine learning capabilities for fraud detection, personalization and operational efficiency. PhonePe's focus on automation has achieved 90% query automation, while Paytm is implementing AI-driven cost optimizations.

The emergence of embedded finance, blockchain applications and cross-border payment solutions presents growth opportunities for both platforms. Their ability to adapt and innovate will determine future market positioning.

Market Value Assessment:

Competitive Landscape Analysis –

The UPI ecosystem continues to grow with 42% year-on-year transaction volume increase to 93.23 billion transactions in 2H 2024. PhonePe and Google Pay command over 82% combined market share, while Paytm holds the third position with declining share.

New entrants like Navi achieving 1% market share and WhatsApp's UPI expansion intensify competitive pressures. This dynamic environment requires continuous innovation and user acquisition strategies.

Revenue Model Evolution –

PhonePe generates revenue through commissions on financial products, merchant services and government UPI incentives contributing 10% of total revenue. The company's diversified revenue streams reduce dependence on single income sources.

Paytm is transitioning to a fee-based model for Soundbox subscriptions, loan distribution and credit card transactions. This shift toward recurring revenue streams aims to improve profitability and reduce transaction-dependent volatility.

Investment and Funding Dynamics –

PhonePe's $850 million funding raised in 2023 from General Atlantic, Walmart, and other investors demonstrates strong institutional support. The company's IPO planning indicates confidence in public market reception.

Paytm's public listing provides access to capital markets but subjects it to market volatility and shareholder expectations. The company's focus on profitability and operational efficiency aims to rebuild investor confidence.

Innovation and Technology Leadership:

Digital Infrastructure Capabilities –

PhonePe has invested extensively in scalable infrastructure capable of handling 250+ million daily transactions. The company's technology platform supports real-time processing with minimal downtime, crucial for maintaining user trust.

Paytm's indigenous payment technology platform incorporates advanced security features and processing capabilities. The company's Soundbox innovation demonstrates product development capabilities beyond basic payment processing.

Customer Experience Enhancement –

Both platforms prioritize user experience optimization through intuitive interfaces and seamless transaction flows. PhonePe's multi-language support in 11 Indian languages enhances accessibility across diverse user segments.

Paytm's comprehensive ecosystem approach integrates payments, commerce, and Financial services, creating sticky user engagement. The platform's diversified service offerings appeal to users seeking consolidated Financial solutions.

Financial Health and Sustainability –

PhonePe's path to profitability demonstrates sustainable business model validation. The company's strong unit economics and operational leverage support long-term Financial health.

Paytm's cost optimization initiatives and revenue diversification indicate management focus on sustainable growth. The company's extensive asset base and ecosystem investments provide multiple pathways to profitability.

Detailed Comparative Metrics:

The comparative analysis reveals PhonePe's dominant market position across key metrics including user base, transaction volume and market share. The company's successful transition to profitability and strong growth trajectory position it favorably for its planned IPO and future expansion.

Paytm's comprehensive ecosystem approach and established market presence provide competitive advantages despite recent regulatory challenges. The company's focus on operational efficiency and revenue diversification indicates potential for sustainable recovery and growth.

The Indian FinTech market's projected growth to $990 billion by 2032 presents substantial opportunities for both platforms. Success will depend on their ability to navigate regulatory requirements, maintain technological innovation and capture emerging market segments.

Future trends likely to shape the competitive landscape include embedded finance adoption, international expansion opportunities, AI-driven personalization and regulatory evolution. Both companies are well-positioned to benefit from India's digital transformation, though their strategic approaches and execution capabilities will determine relative market positioning.

Arin Sahu

FinTech Specialist

Asiatic International Corp

Instagram- https://shorturl.at/Rq56s

Youtube- https://www.youtube.com/aerosoftcorp