AI in Banking: The Smart Revolution You Can’t Ignore

AI in Banking, Artificial Intelligence in Banking sector, Machine Learning in Banking, Future of Digital Banking, Banking Automation

The Future of Banking? It’s Already Here.

“Imagine a Bank that Anticipates your needs, stops Fraud before it strikes, and offers you a Loan exactly when you’re ready — all without you lifting a finger.”

Welcome to the world of AI-Powered Banking, where Algorithms, not just Bankers, are working tirelessly to keep your Money Safe and your life easier.

What Does AI in Banking Really Mean?

In simple words:

AI in Banking is when Banks use smart Algorithms, Machine Learning, and Data-Crunching tools to Work Faster, Think Ahead, and Serve you Better.

It’s like having an invisible Banker working 24x7 — spotting Fraud, approving Loans, and even Planning your Financial Future.

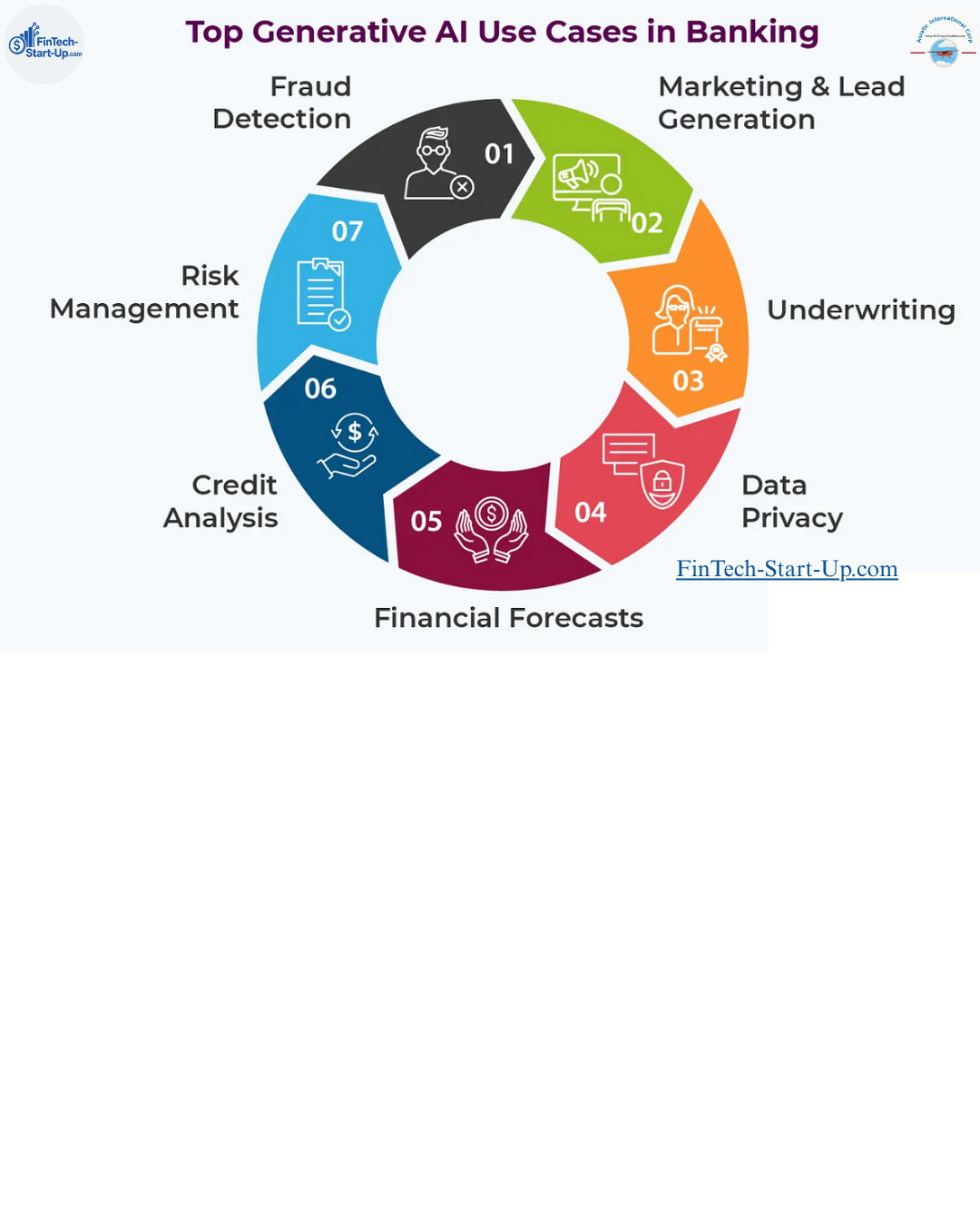

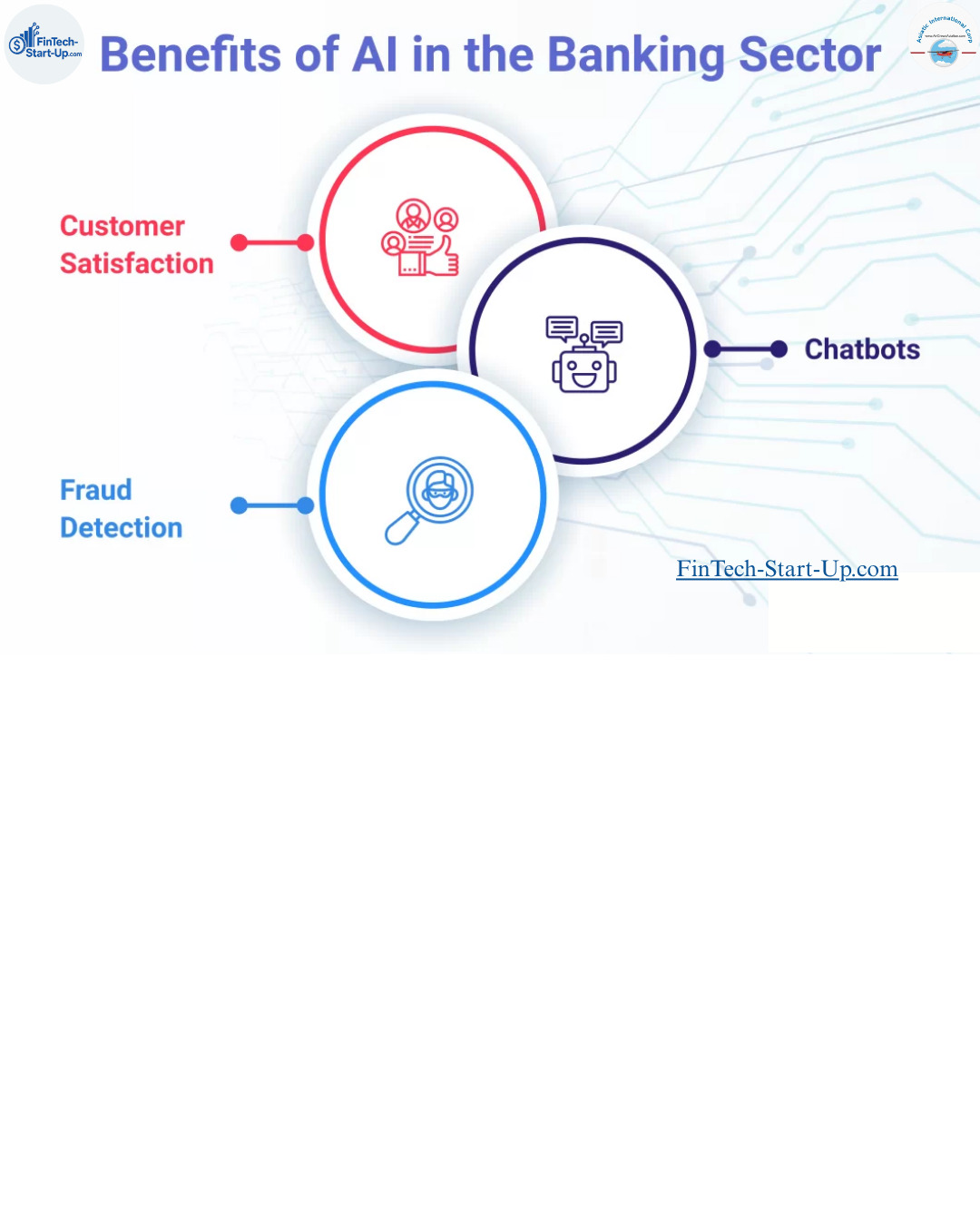

Where Is AI Making Waves in Banking?

1. Stopping Fraud Before It Happens

Banks process Millions of transactions every day. AI watches each one like a hawk — catching suspicious activity in milliseconds.

Think of it as a Personal BodyGuard for your Money.

2. Chatbots: Your 24/7 Digital Bank Buddy

Gone are the Days of long waits on Customer-Care lines.

AI ChatBots like SBI’s SIA or ICICI’s iPal can instantly help you check balances, block cards, or even apply for loans — all while you sip your coffee.

3. Smarter Loans & Credit Decisions

Forget rigid Old-School credit scores.

AI looks at Thousands of Data Points — from your Payment History to spending patterns — to decide if you’re a good bet.

Result? Faster approvals and more People getting access to Credit.

4. Hyper-Personalized Banking

Imagine your Bank telling you:

“Hey, based on your spending, how about we move ₹5,000 into a High-Yield Savings Account this month?”

AI turns Banking from generic to Tailor-Made just for you.

5. Automation: No More Tedious Paperwork

AI + Robotic Process Automation (RPA) handles boring tasks like Verifying KYC documents or generating Compliance Reports.

Banks save time, you get quicker service.

Real-World Examples: Not Sci-Fi, Real Life

JP Morgan uses AI to read complex contracts — saving lawyers 360,000 hours a year.

HDFC Bank uses AI to sniff out Fraud across credit card transactions instantly.

Bank of America’s Erica serves over 25 million customers, handling Queries and offering smart Financial tips.

The Road Ahead: AI Will Make Banking Feel Like Magic

Predict & Prevent: Your Bank might warn you before you’re about to OverDraft.

Talk & Transact: Just tell your Phone, “Pay my Electricity Bill,” and it’s done.

Facial & Voice Security: Your Face or Voice will unlock Transactions — goodbye Passwords!

The next Banker you meet might not wear a suit — it could be an algorithm that knows your dreams better than you do.

Trisha Kesarwani

Fintech Specialist

Asiatic In Corp

LinkedIn -

https://fs.blabigo.com/s/3mjdTRUA

Vcard:

https://linko.page/svhhsuwbth0t